In This Article

LOANS

When someone takes out a loan in order to buy a property, it is called a purchase money mortgage. The most common loan aside from the purchase money mortgage, is the refinance loan. This is when someone takes out a new loan on a property that he already owns. A person refinances for many reasons, and the risks involved in refinancing are different than those for a purchase money mortgage. This blog discusses some of the unique aspects of the refinance loan.

Refinancing Your Mortgage

Refinancing means taking out a new loan that replaces an existing loan on a property. In a sense, the process of refinancing renews the property to the owner. It can be understood as selling the building to the bank and then buying it back under a new loan arrangement. The balance of the old loan is absorbed by the new one.

Reasons to Refinance Your Mortgage

There are three general reasons that a client may want to refinance:

- The previous loan term expired.

- The average term of a commercial real estate mortgage is five, seven, or ten years, payable on a 25-30 year amortization schedule. This means that the monthly payments are scheduled as if the loan would be paid off in 30 years. However, the interest rate is only locked for the life of the loan, which is five, seven, or ten years.

Most banks offer options that when the term ends, the loan can be extended at a predetermined rate. Since this rate is usually higher than the market rate, most people choose to refinance their loan at the end of a term rather than accepting the bank’s option.

- The average term of a commercial real estate mortgage is five, seven, or ten years, payable on a 25-30 year amortization schedule. This means that the monthly payments are scheduled as if the loan would be paid off in 30 years. However, the interest rate is only locked for the life of the loan, which is five, seven, or ten years.

- To lower the monthly payments.

- When interest rates go down significantly from the time that the loan was taken out, it may be possible to lower one’s monthly payments by refinancing with the new rate. Any such calculation should include the costs of the refinance itself, i.e., closing costs and related fees.

For example, someone took out a twenty-five-year mortgage at 12%, and is paying $1200 per month. Ten years later, interest rates for 15-year loans stand at 6%. Refinancing them will reduce his monthly payment from $1200 to $844.

- When interest rates go down significantly from the time that the loan was taken out, it may be possible to lower one’s monthly payments by refinancing with the new rate. Any such calculation should include the costs of the refinance itself, i.e., closing costs and related fees.

- To cash out.

- As the rents in a property increase over time, so does the equity, or value, of the property. This added value can be borrowed against the owner of the property.

Even if the property value did not rise, since he has been paying the mortgage for some time, an owner is able to cash out by renewing the loan. For example, someone who has a mortgage of $500,000 takes out a new mortgage for $800,000. Even after allowing for closing costs of $20,000, the owner cashes out $280,000. A real estate investor usually takes out this money to reinvest in other real estate.

- As the rents in a property increase over time, so does the equity, or value, of the property. This added value can be borrowed against the owner of the property.

Prepayment Penalty on Your Mortgage

A bank, upon setting up a loan, relies on the monthly payments of the principal plus interest in a timely manner for the remainder of the term. If a borrower pays the loan before the term finishes, the bank cannot collect the interest on the loan for the time between the payment of the debt and the end of the term. The bank, therefore, charges the borrower a penalty, called a prepayment penalty (PPP), to address this loss.

There are three formulas commonly used to calculate the PPP. They are structured so as to accurately assess and balance out the loss that the bank takes on the prepayment. The bank decides which prepayment penalty method they will use, not the borrower.

Sliding Scale

Since the loss to the bank diminishes as the end of the term approaches, the bank, using the sliding scale formula, penalizes less for each passing year. In brokerage terminology, this formula is also called the “5,4,3,2,1”.

In a five-year term, a borrower will be charged 5% of the loan balance for prepaying in the first year, 4% for prepaying in the second year, 3% in the third, etc. During the last 60-90 days of a loan, the bank will usually allow a borrower to pay off the loan without incurring any penalty. When the term is longer than five years, the penalty is increased proportionately for the duration of the term.

When interest rates go down, the sliding scale schedule is not so prohibitive as to prevent a borrower from paying off the existing loan to take advantage of lower rates. As always, the appropriate calculations must be made to account for penalties and closing costs.

For example, a client took out a loan with a 9% rate. Now, with three years left to the loan, rates fall to 6.5%, and the client wants to pay off his old loan and take out a new one at the present rate. His penalty of 3% will be recouped in approximately 14 months with the money that he saves due to the lower rate, and he continues to enjoy the lower rate for the rest of the loan term.

Yield Maintenance

Yield maintenance is the present value (PV) of future cash flows. This means that the bank charges the full amount of interest that it could have made on the balance of the loan. Since the bank can use the prepaid principle to buy Treasuries and thus make some profits on this money, the yield that Treasuries will give for the remainder of the term is deducted from the penalty.

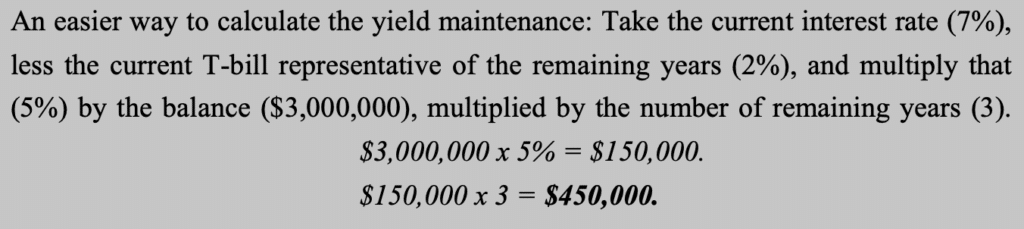

To illustrate: For a loan of $3,000,000 at 7% for a ten-year term, the annual payments are at least $210,000 ($3,000,000 x 7%). [To keep the illustration simple, assume that the borrower only paid the interest, not the principle.] If the borrower pays the balance with three years left on the loan, the bank loses $630,000 in interest ($210,000 x 3). However, with the repaid principle, the bank can buy three-year Treasury bills at, for example, 2.00%. On the $3,000,000 balance, this amounts to a profit of $60,000 for three years, or $180,000. Thus, the penalty in this case would be $450,000.

The yield maintenance formula usually makes refinancing prohibitively costly. However, if the value of the property has gone up significantly, and the rates that the Treasury bills are trading are not too far from the actual current rate, a borrower can consider cashing out even with the yield maintenance PPP.

There is a minimum 1% penalty with the yield maintenance formula.

WE CAN HELP

GPARENCY provides access to a range of features that can help investors navigate the complex world of commercial real estate and stay ahead of the curve, including:

Free equity introduction: GPs (general partners) can let us know which deal they’re looking to take partners on and our team will send it out to our entire network of accredited LPs.

Close any deal on your terms: get our members-only brokerage pricing of $11K upfront or ¼ point at closing.

50M+ data references so you’re always prepared: Our digital marketplace provides you with up-to-date information on commercial real estate listings so you can make informed investment decisions.

50,000+ commercial listings: find your next acquisition with our easy-to-use interactive map and street view displays.Expert assistance each step of the way: Our team of commercial real estate veterans are available to answer any questions you may have about the financing process.

FAQs:

- Why do banks charge prepayment penalties?

- Banks charge prepayment penalties to protect themselves from potential financial losses that can arise when a borrower pays off a loan before its scheduled maturity date. These penalties are usually a percentage of the remaining balance on the loan, and the amount can vary depending on the terms of the loan.

When a borrower repays a loan early, the lender loses out on the interest income it would have received if the borrower had made all of the scheduled payments. This can be a significant loss, especially for long-term loans with high-interest rates. Prepayment penalties are intended to compensate the lender for this lost income.

It’s worth noting that prepayment penalties are not always charged on loans. Some loans, such as mortgages, may have prepayment penalty clauses that allow borrowers to prepay without penalty after a certain period of time. However, in general, prepayment penalties are designed to protect the lender’s financial interests and help maintain the stability of their loan portfolio.

- Banks charge prepayment penalties to protect themselves from potential financial losses that can arise when a borrower pays off a loan before its scheduled maturity date. These penalties are usually a percentage of the remaining balance on the loan, and the amount can vary depending on the terms of the loan.

- How do you know if a loan is a wise investment?

- Determining whether a loan is a wise investment requires careful analysis and consideration of several factors, including:

- Interest rates: Consider the interest rate of the loan and compare it to current market rates. If the interest rate is significantly higher than average, it may not be a wise investment.

- Loan terms: Look at the terms of the loan, including the length of the repayment period, fees, and penalties. Consider whether the terms are reasonable and whether they fit your financial goals and circumstances.

- Purpose of the loan: Consider the purpose of the loan and whether it will generate a return on investment. For example, if you are taking out a loan to start a business or invest in real estate, consider the potential profitability of these ventures.

- Creditworthiness: Evaluate your own creditworthiness and determine whether you are likely to qualify for the loan. Consider whether you will be able to make the payments on time and whether you have the resources to pay off the loan if necessary.

- Risk vs. reward: Assess the risk and potential reward of the loan. Consider the potential benefits of the loan against the potential risks and determine whether the potential reward is worth the risk.

- Determining whether a loan is a wise investment requires careful analysis and consideration of several factors, including:

Ultimately, a wise investment loan is one that fits your financial goals and circumstances, has reasonable terms, and provides a return on investment that outweighs the risks. It’s important to carefully consider all factors and do your research before taking out a loan to ensure that it is a wise investment.