In this article

As a commercial building owner, it’s important to understand mortgages and how banks evaluate property when deciding on loan approvals. While the exact process is slightly different from bank to bank, there are key factors that can help you better understand what lenders take into account for mortgage applications and where your focus should be as you apply for financing.

To guide you through this vital step in the loan approval process, we’ll explain each of these lender considerations in detail so that you can feel more confident when it comes time to secure capital.

Banks make money in one of two ways.

1) They charge you a fee upfront as a percent of the loan amount. For example, they may charge you a flat fee of $10,000 on a $1 million loan (which is 1% of the amount of the loan).

2) The other way banks make money is on the profit of the interest rate. For example, if the bank charges 6% interest, and if their total cost of money, including overhead, is 5.5%, then the bank makes half a percent a year as profit.

Now, while the interest represents a potential gain for the bank, there is also a considerable risk inherent in lending out large sums of money. What if the borrower cannot afford to make the mortgage payments (this could happen for various reasons) and defaults (stops payments) on the loan? What measures can a bank take to protect itself from these risks?

Most banks approach lending with a two-pronged safety strategy. First of all, a bank makes sure, before it lends out its money, that the property that is being borrowed against has the capacity to produce the revenue necessary to pay for the loan. The actual process of the bank’s evaluation of a mortgaged property is the subject of this blog.

Secondly, the bank assures itself that should the loan default, the bank’s mortgage would be covered by the proceeds of the sale of the property. This process is called foreclosure.

Cash Flow Lenders

Cash flow lenders rely on profits from monthly interest payments on the loans that they make out. They are, therefore, primarily focused on the cash flow that the mortgaged property can produce. Most banks are cash-flow lenders. The bank performs much research into the property to ensure that it can produce enough cash flow to service the debt and that there will be enough net operating income (NOI) or profit for the owner to take home after the mortgage is paid. The bank will not lend the money if the projected cash flow covers only the debt service.

Why, as long as there is enough to cover the debt, should the bank care about the owner’s extra NOI or profit? For one, if the bank were to calculate the cash flow to exactly cover the debt, it would not leave any room for the chance of a drop in income or increase in expenses. In order to keep some cushion, the bank requires more cash flow than would actually be necessary to pay the debt service.

Furthermore, the bank is concerned that the owner makes a profit on his investment. An owner who is not making a profit on his building is not inclined to put in the effort to push the property through any potentially difficult situation. He may decide in a crunch that instead of dealing with a non-profitable building, he will stop paying the mortgage and let the bank take it back.

There is a common misconception that a bank’s objective is to profit from individuals who are unable to repay their loans and repossess them.That’s not the goal. The goal is for the bank to make money without any headaches. Think of a bank in terms of one who rents out money, similar to how car dealerships operate. Just as car dealerships rent out cars to you to use for a specific amount of time, the bank rents money to you to use for a specific time period. During the time of your rental, you are paying the bank for the use of the money.

A cash flow lender, however, is in the business of making money from monthly mortgage payments, not from selling foreclosed properties. Since the bank does not want to deal with foreclosures, it has a vested interest in ensuring that the owner can make a profit from the proposed property.

Due Diligence

Just as it is in the owner’s best interest to perform all the due diligence to assure that the acquisition will not bring him a loss, the same is true for the bank. Therefore, the bank also takes all of the precautions that a prospective owner takes before buying a property. If the buyer has a great property and makes a lot of money, then he will most likely pay the bank back sooner than anticipated.

The bank makes its own assessment regarding the income and expenses of the property. It reviews the tenancy to ensure that the property has a sufficient number of long-term tenants and new tenants. For example, if the property is multi-family, the bank would want to know the number of tenants that have lived there for a long time, the number of tenants that are new, and how long units typically go unrented before a new tenant moves in. For a retail store, the bank would want the information on anchor and credit tenants and which tenants have been in that location for some time. The bank would desire similar information for office buildings or industrial buildings. Long-standing tenants mean that they were successful in this location and will likely renew their lease when it expires. This means fewer TI (tenant improvement) dollars, fewer LC (leasing commission) costs, and no downtime between tenants.

Generally, those conditions which indicate stability and profit for the owner are the same for the lender. A landlord making money on a building will pay the mortgage punctually and will put sufficient effort into the property’s continued success.

Bankers’ View of a Mortgage

While both the bank and the buyer are looking at the same property, they may not always see eye to eye about what constitutes a good investment. In a typical acquisition, the bank puts much more money on the line than the buyer does. While an owner may look for speculation on future profits, the bank looks at the risk. The bank looks at a property assessing the risk in the event that the owner defaults on his loan and they have to take it over and run it. This is why banks are, therefore, more conservative in their lending outlook. They will not allow for any major speculation when making calculations of future increased cash flow compared to previous years. A bank’s calculations are always based on the most conservative scenario.

Mortgage and the Debt Service Coverage Ratio

How much profit must the bank see above the debt service before they will lend? Banks have developed a formula to calculate this amount, called the Debt Service Coverage Ratio (DSCR). It is the ratio of the NOI to the amount of the debt service.

Let’s delve into the specifics of a particular building to provide a clearer understanding of the Debt Service Coverage Ratio (DSCR). Consider an example where we have a commercial property valued at $1,000,000. This property generates a Net Operating Income (NOI) of $72,967, while the associated debt service amounts to $42,967.

By calculating the DSCR, which is the ratio of NOI to the debt service, we find that it is 1.7x. This means that after fulfilling the debt obligations, the property owner is left with 1.7 times the amount of the debt service, resulting in a profit margin of 70% (in this case, $30,000). Generally, banks typically require a DSCR between 1.2x and 1.3x to consider a loan secure. In this example, with a DSCR of 1.7x, the loan for this specific building would be deemed highly secure.

For example, if the debt service coverage is $42,967, and the NOI is $72,967, then the DSCR is 1.7x. In other words, after servicing the debt, the owner is left with 1.7 times the amount of the debt service, which works out to 70% of the amount of the debt service as profit; in this case, $30,000.

The DSCR required by most banks is between 1.2x and 1.3x. The above example would be considered a very secure loan for a bank since it has a DSCR of 1.7x.

Appreciating Concepts: Debt Service Constant

In the above discussion regarding debt service coverage, the amount given for the debt service did not change annually. In order to calculate the DSCR, you must have a debt service amount that is constant. However, banks need to use a special calculation called the debt service constant to keep the debt service constant.

Without the debt service constant, a different loan amount would be paid every year. This is because every year the amount of interest changes every year since the interest is paid on less and less principal. For example, a loan of $750,000 is borrowed at 4% interest and scheduled to be paid up at the end of 30 years (self-amortize by the end of 30 years). At the end of the first year, the borrower would pay $30,000 interest ($750,000 x 4%), in addition to 1/30 of the principal ($25,000). Total payment for the first year: $55,000.

At the end of the first year, the principal was reduced to $725,000. 4% interest on $725,000 is $29,000. With an additional 1/30 ($25,000) of the principal, the second

At the end of the first year, the principal was reduced to $725,000. 4% interest on $725,000 is $29,000. With an additional 1/30 ($25,000) of the principal, the second year’s payment would be $54,000, an $1,000 decrease from the previous year’s payment.

The declining system of payment can be viewed differently by the borrower and the lender. The borrower may prefer lower payments at the beginning of the loan and higher payments towards the end to ease their initial financial burden. On the other hand, the lender may prefer a more consistent and streamlined approach to facilitate budgeting. However, amortization can address these differing preferences by structuring loan payments to gradually reduce the principal amount over time while ensuring a consistent payment schedule.

The debt constant percent is a calculation used to figure out a constant amount that a borrower can pay and have the loan paid up by the end of the term. Each loan amount, interest rate, and payment schedule has a percent number, which, when applied to the loan amount, yields the debt service constant for that loan.

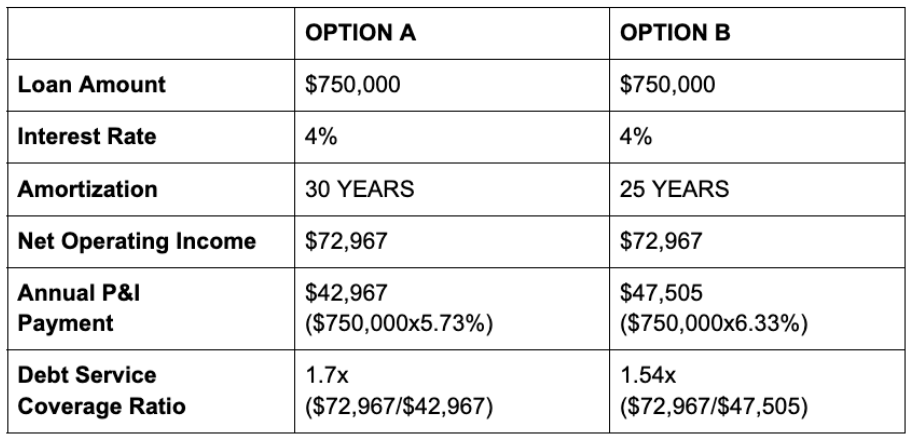

The DSC for $750,000 at 4% for 30 years is 5.73x. Multiplying $750,000 by 5.73% yields $42,967. By paying even annual payments of $42,967, the borrower’s balance will be fully paid by the end of the 30 years.

The following chart illustrates the relationship between the constant and the DSCR for a 30-year amortization vs. a 25-year amortization.

Reserves

A prudent landlord always puts away money on a regular basis to cover large, non-recurring expenses that can come up. These expenses include structural repairs, such as a new roof or repair of the facade, or purchasing new appliances for his tenants in the case of a multifamily property. Another common expense is the TIs (Tenant Improvements) and LCs (Leasing Commissions) for tenants who do not renew their leases. If the owner has money put away for these occasions, he will be able to absorb the costs of paying for these expenses without having to neglect his other regular expenses.

Often, landlords are not so prudent. When a bank lends money, it is concerned that the owner will not have money set aside for these expenses. In that case, when a large expense does come up, the owner has to pay out of pocket and may not be able to keep up with the mortgage payments as well. The bank, however, does not wait for this to happen. As part of the arrangement of the loan, a bank collects a certain amount for reserves each month. This is money earmarked for various non-recurring expenses and put away in an escrow account. This money does not belong to the bank. The bank merely collects and holds the money so that it should be available to the landlord when he needs it. When the landlord wishes to withdraw this money for the expense it was designated for, he submits a bill to the bank, and the bank releases the funds.

Equity

One reason that a bank will not lend out 100% of the money necessary for the purchase is that the banks want the borrower to be personally invested in the success of the property. An owner who did not invest any of his own money into a property may be inclined to walk away from it at the first difficulty. But an owner with a considerable amount of personal funds invested in the building will look after the success of the property because it is his own money at stake.

Typically, a bank wants the owner to have 25% equity in a building at all times. That is, to have 25% ownership of the property after all debts. Thus, when buying a commercial property for $1,000,000, the buyer would put a down payment of 25% of the purchase price ($250,000) and finance the remaining 75% ($750,000).

The percentage of the cost of the property that a bank is willing to lend on is called Loan To Cost (LTC). A bank that lends on a 75% LTC would only lend up to 75% of the total purchase price. In this way, the buyer is forced to pay for the remaining 25% from his own resources., thus ensuring that he retains 25% equity in the building.

FAQs

- What is a foreclosure?

- Foreclosure is the legal process by which a lender repossesses a borrower’s property when the borrower is unable to make their mortgage payments as agreed. Foreclosure proceedings can be initiated by the lender when a borrower is behind on their mortgage payments and cannot resolve the issue through other means, such as loan modification or refinancing.

- What is debt service?

- Debt service is the amount necessary to service or pay the monthly bills for both the principal and the interest of the debt.

- What is the debt service coverage ratio?

- Debt Service Coverage Ratio (DSCR) is a financial metric used to determine the ability of a borrower to pay off their debt obligations. It is calculated as the ratio of a borrower’s net operating income (NOI) to their total debt service, which includes both principal and interest payments. A DSCR of 1.0 means that a borrower’s net operating income is equal to their debt service, and anything greater than 1.0 indicates that a borrower is generating enough income to cover their debt payments plus have some left over. A DSCR of less than 1.0 indicates that a borrower is not generating enough income to cover their debt service and may struggle to make their debt payments.

- What is the debt service constant?

- The debt service constant, also known as the loan constant, is a financial metric that represents the fixed loan payment that a borrower is required to make each year as a percentage of the loan amount. It is a constant, meaning it remains the same throughout the term of the loan, regardless of changes in interest rates or the balance of the loan. The debt service constant is used to calculate the amount of debt service that a borrower is required to pay each year.

- Is it better to borrow from a conventional bank or another lending institution?

- The choice between borrowing from a conventional bank or another lending institution for commercial real estate depends on factors such as interest rates, eligibility criteria, speed of financing, relationship and services offered, specialized expertise, and flexibility. Conventional banks may have competitive rates and comprehensive banking services, but alternative lenders might provide more flexible terms, faster approval processes, and specialized knowledge in specific real estate sectors. Consider your specific needs and priorities before deciding on the best option for your commercial real estate borrowing.